38 duration zero coupon bond

2022 CFA Level I Exam: CFA Study Preparation The Macaulay duration of a zero-coupon bond is its time-to-maturity. The Macaulay duration of a perpetual bond (perpetuity) is (1 + r) / r. Coupon rate is inversely related to Macaulay duration and modified duration. Yield-to-maturity is also inversely related to Macaulay duration and modified duration. Portfolio Duration and its Limitations | CFA Level 1 - AnalystPrep There are just 2 future cash flows in the portfolio, which are the redemption of the principal of the 2 zero-coupon bonds. However, in more complex portfolios, a series of coupon and principal payments may occur on various dates. ... D i = duration of bond i. n = number of bonds in portfolio. Using the above data, we can calculate portfolio ...

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Duration zero coupon bond

Bond (finance) - Wikipedia In finance, a bond is a type of security under which the issuer owes the holder a debt, and is obliged - depending on the terms - to repay the principal (i.e. amount borrowed) of the bond at the maturity date as well as interest (called the coupon) over a specified amount of time.Interest is usually payable at fixed intervals (semiannual, annual, and less frequently at other periods). Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months. Duration Definition - Investopedia The duration of a zero-coupon bond equals its time to maturity since it pays no coupon. Duration Strategies In the financial press, you may have heard investors and analysts discuss long-duration...

Duration zero coupon bond. Zero Coupon Bond Calculator - MiniWebtool The Zero Coupon Bond Calculator is used to calculate the zero-coupon bond value. Zero Coupon Bond Definition. A zero-coupon bond is a bond bought at a price lower than its face value, with the face value repaid at the time of maturity. It does not make periodic interest payments. When the bond reaches maturity, its investor receives its face value. The Macaulay Duration of a Zero-Coupon Bond in Excel Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and... fixed income - Duration of callable zero coupon bond - Quantitative ... What is the bond duration? A- 10 Years B- 5 Years C- 7.5 Years D- Cannot be determined based on the data given. According to me it should be 10 years as the duration of a zero coupon bond is always equal to its maturity. But I am not getting convinced with my answer because of the callable feature in the question. Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond . Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

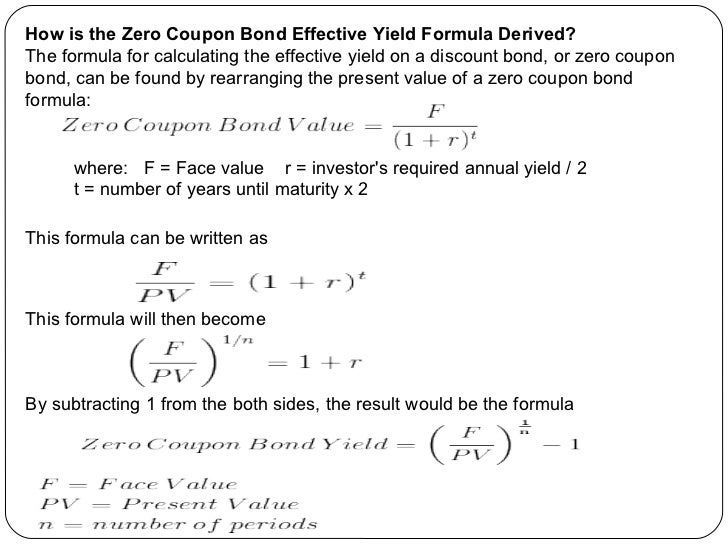

Zero Coupon Bond Value - Formula (with Calculator) A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. duration of zero coupon bonds | Forum | Bionic Turtle With respect to a zero coupon bond, Macaulay duration = maturity, and therefore must be a monotonically increasing function of maturity. On the other hand, DV01 of a zero (or deeply discounted) is not strictly increasing as DV01 = P*D/10,000 and the numerator has offsetting effects. If you'd kindly reference, I can fix? Thanks! Apr 7, 2012 #3 S Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding Zero-coupon bond - Wikipedia A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years. For some Canadian bonds, the maturity may be over 90 years.

Zero Duration ETF List - ETF Database zero duration and all other bond durations are ranked based on their aggregate 3-month fund flows for all u.s.-listed bond etfs that are classified by etf database as being mostly exposed to those respective bond durations. 3-month fund flows is a metric that can be used to gauge the perceived popularity amongst investors of zero duration … Modified duration of zero-coupond bond (FRM practice question ... - YouTube A zero-coupon bond with maturity of ten (10) years has a 6% bond-equivalent yield (semi-annual compounding). What is the bond's modified duration? Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ So a 10 year zero coupon bond paying 10% interest with a $1000 face value would cost you $385.54 today. In the opposite direction, you can compute the yield to maturity of a zero coupon bond with a regular YTM calculator. Zero Coupon Bond Modified Duration Formula | Bionic Turtle We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%.

PPT - Chapter 7 The Valuation and Characteristics of Bonds PowerPoint ...

Macaulay Duration - Overview, How To Calculate, Factors A zero-coupon bond assumes the highest Macaulay duration compared with coupon bonds, assuming other features are the same. It is equal to the maturity for a zero-coupon bond and is less than the maturity for coupon bonds. Macaulay duration also demonstrates an inverse relationship with yield to maturity.

The Allure Of Zero Coupon Municipal Bonds: A Low Risk Investment With ...

Solved The duration of a zero‑coupon bond is always - Chegg.com Question: The duration of a zero‑coupon bond is always _____ its maturity. The duration of a coupon bond is always _____ its maturity. A. equal to; less than B. greater than; equal to C. greater than; less than D. equal to; equal to. This problem has been solved! See the answer See the ...

ZERO COUPON BOND CALCULATOR - BOND CALCULATOR - AIR MILE CALCULATOR

Zero Coupon Bond | Investor.gov Zero Coupon Bond. Zero coupon bonds are bonds that do not pay interest during the life of the bonds. Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. The maturity dates on zero coupon bonds are usually long-term—many don't ...

Calculator Zero Coupon Bond - CALCULUN

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Finding YTM of a Zero Coupon Bond (6.2.1) - YouTube

Bond Duration Calculator - Macaulay and Modified Duration - DQYDJ From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity - it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

Modified duration of zero-coupond bond (FRM practice question) - YouTube

What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

3. How to calculate a zero coupon bond, coupon bond prices with Program ...

Default Risk and the Duration of Zero Coupon Bonds This paper applies a contingent claims approach to examine the duration of a zero coupon bond subject to default risk. One replicating portfolio for a default-prone zero coupon bond contains a long position in the default-free asset plus a short position in a put option on the underlying assets. The duration of the bond is shown to be a ...

Macaulay's Duration, a Second Look - GlynHolton.com

PDF Duration - New York University Duration 12 Example: Zero-Rate Dollar Duration of a Coupon Bond The zero-rate dollar duration of $1 par of a T-year bond with coupon rate c is This is the dollar price sensitivity to a parallel shift in the zero yield curve. Example: dollar duration of $1 par of a 1-year 6%-coupon bond: € c 2 [0.5 (1+r 0.5 /2) 2 + 1 (1+r 1 /2) 3 + 1.5 (1+r 1 ...

When do key rate measures add up? - Scanrate

Macaulay's Duration | Formula | Example - XPLAIND.com Duration of Bond A is 4.5, i.e. the maturity period (in years) of the zero-coupon bond. Duration of Bond B is calculated by first finding the present value of each of the annual coupons and maturity value. Annual coupon is $50 (i.e. 5% of the $1,000) and the maturity value is $1,000.

Zero Coupon Bond - YouTube

Solved What will be the duration of a zero coupon bond - Chegg We review their content and use your feedback to keep the quality high. 100% (1 rating) ANSWER - Duration of Zero coupon bond (ZCB) is the maturity time of the bond is 5 years. Basically duration of the bond is the time at which the payments received …. View the full answer.

Bond’s Maturity, Coupon, and Yield Level | CFA Level 1 - AnalystPrep

Duration Definition - Investopedia The duration of a zero-coupon bond equals its time to maturity since it pays no coupon. Duration Strategies In the financial press, you may have heard investors and analysts discuss long-duration...

Bonds ppt

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

Bond valuation

Bond (finance) - Wikipedia In finance, a bond is a type of security under which the issuer owes the holder a debt, and is obliged - depending on the terms - to repay the principal (i.e. amount borrowed) of the bond at the maturity date as well as interest (called the coupon) over a specified amount of time.Interest is usually payable at fixed intervals (semiannual, annual, and less frequently at other periods).

Solved: 1 An Investor Purchases A Zero Coupon Bond With 12... | Chegg.com

How to Calculate the Yield of a Zero Coupon Bond Using Forward Rates?

Floating Rate Notes (FRNs) Valuation | Floating Rate Bonds Pricing ...

united states - Can zero-coupon bonds go down in price? - Personal ...

Post a Comment for "38 duration zero coupon bond"